by Andrew Lam. Andrew is the author of two books of personal essays: “Perfume Dreams: Reflections on the Vietnamese Diaspora,” and “East Eats West: Writing in Two Hemispheres,” and a book of short stories, “Birds of Paradise Lost.” This article was originally published by the Center for Health Journalism.

by Andrew Lam. Andrew is the author of two books of personal essays: “Perfume Dreams: Reflections on the Vietnamese Diaspora,” and “East Eats West: Writing in Two Hemispheres,” and a book of short stories, “Birds of Paradise Lost.” This article was originally published by the Center for Health Journalism.

The cost of aging in America is exorbitant, which my siblings and I are finding out firsthand through our struggles over the past three years to take care of our aged parents.

My mother, suffering from Alzheimer’s, spends her remaining days mostly in a hospital bed in hospice care, but mercifully next to my father. Both live in an apartment in a high-end assisted living compound in Fremont, California.

It hadn’t been easy to get them to this apartment, to say the least. After an epic struggle to get their coverage under long-term care insurance activated (my father had the wherewithal to buy such coverage for himself and my mother while working for the Port of Oakland many years ago) our family still faces a gap in the monthly budget.

The cost of hospitalization and emergency visits alone for both are in the tens of thousands for each of them, just in the last three months. And the cost of assisted living for both is around $14,000 a month, a figure that only increases as more services are required.

My parents’ story is part of a growing crisis. According to a 2016 study from the Department of Health and Human Services, 52 percent of Americans turning 65 today will require long-term care services during their lifetimes. About 12 percent will need between two and five years of long-term care, and nearly 14 percent will require five or more years — that’s one out of every seven adults. Such extended care can quickly dwindle savings and lead to bankruptcy, while placing tremendous pressure on family members forced to double as caregivers and health advocates.

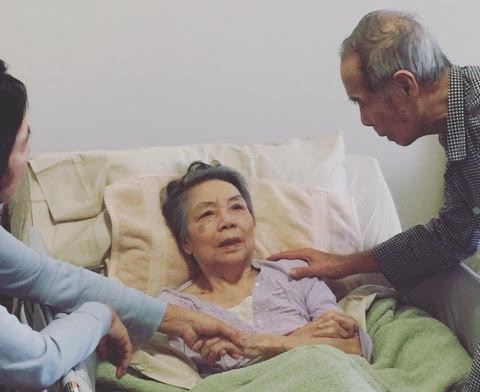

The author’s mother, surrounded by family members. (Photo courtesy Andrew Lam)

As it is, both my parents can barely pay for these stratospheric healthcare bills and assisted living even with Medicare and my father’s long-term care insurance, which only pays half of their monthly bill. And what is not mentioned in the formula when costs are calculated is this crucial factor: family ties and support.

Indeed, hidden behind my parents’ relatively good fortune is an asset sociologists call human capital — something that they couldn’t possibly do without. In my parents’ case it’s consisted of their three adult children working together. Without us — and especially without my devoted sister, who as my parents’ legal guardian works tirelessly to pressure their insurer for payment and fights for every detail of their health care on the daily basis — I can confidently say that both would have been dead by now.

My sister makes sure doctors and nurses pay attention to their eating habits, pay attention blood pressure changes, that my parents get their medical checkups on time, and she demands blood tests, X-rays, and hospice care for my mother — services that are available but only if requested.

And still, it remains a constant struggle. If long-term care insurance has saved my parents from complete destitution in old age, it still falls short of the overall cost to keep them at the assisted living facility. All their monthly income — retirement, investment interests, social securities, you name it — now goes to pay the remainder left over after insurance, which covers less than two-thirds of their bills. The costs keep rising, chipping away at what remains of my parents’ personal savings.

We three adult children visit as often as we can to keep my parents’ company. And it helps that, being close to the second largest Vietnamese American community in Santa Clara, my parents have many guests who visit them on a regular basis.

It makes me shudder to think what it would have been like had my parents struggled alone, without financial backing and a support system? As is the case for many others, it surely would have shaved years off their lives.

All things considered, my parents are faring much better than others in their age group within their community. None of my father’s friends, for instance, bought long-term care insurance. Many now live in crowded convalescent homes, three people to a room, and with little support system, while others put tremendous pressure on their adult children who take care of them at home.

A friend I know gave up his job working at a tech company to take care of his mother full time. Another friend gave up his job as a journalist to take his mother home to Vietnam so that she would have round the clock care and in her language. She too suffered from Alzheimer’s, and he did not want to put her in a home full of strangers.

The examples are endless.

And the costs are staggering. According to Paying for Senior Care, the average cost for assisted living in the San Jose area in California is $4,825 a month, a figure that rises to $8,850 for nursing care. And according to the Genworth Financial, which tracks the costs of long-term care, the bill for a private room in a nursing home is around $91,250 a year in 2015.

All these expenses are before human capital is factored in. My sister, for instance, who lives in a different city an hour drive away, easily spends 18 hours a week caring for my parents. The stress is tremendous. According to a study by Indiana University Center for Aging Research in Indianapolis, caregivers often experience stress while helping their loved ones. Decision-makers had fairly high levels of anxiety and depression while their relative was hospitalized. About half had moderate to severe depression, and 14 percent had symptoms of PTSD.

This all seems like a nightmare for any baby boomer facing retirement with the hope of leaving something behind for their children, besides stress and PTSD. For immigrants like my parents, who toiled for over three decades in America before retiring and who are lucky enough to have children advocating for their well being, the American Dream still fades further away the moment each health care bill arrives in the mail.

The opinions expressed in this article are those of the author and do not necessarily reflect those of the Diverse Elders Coalition.